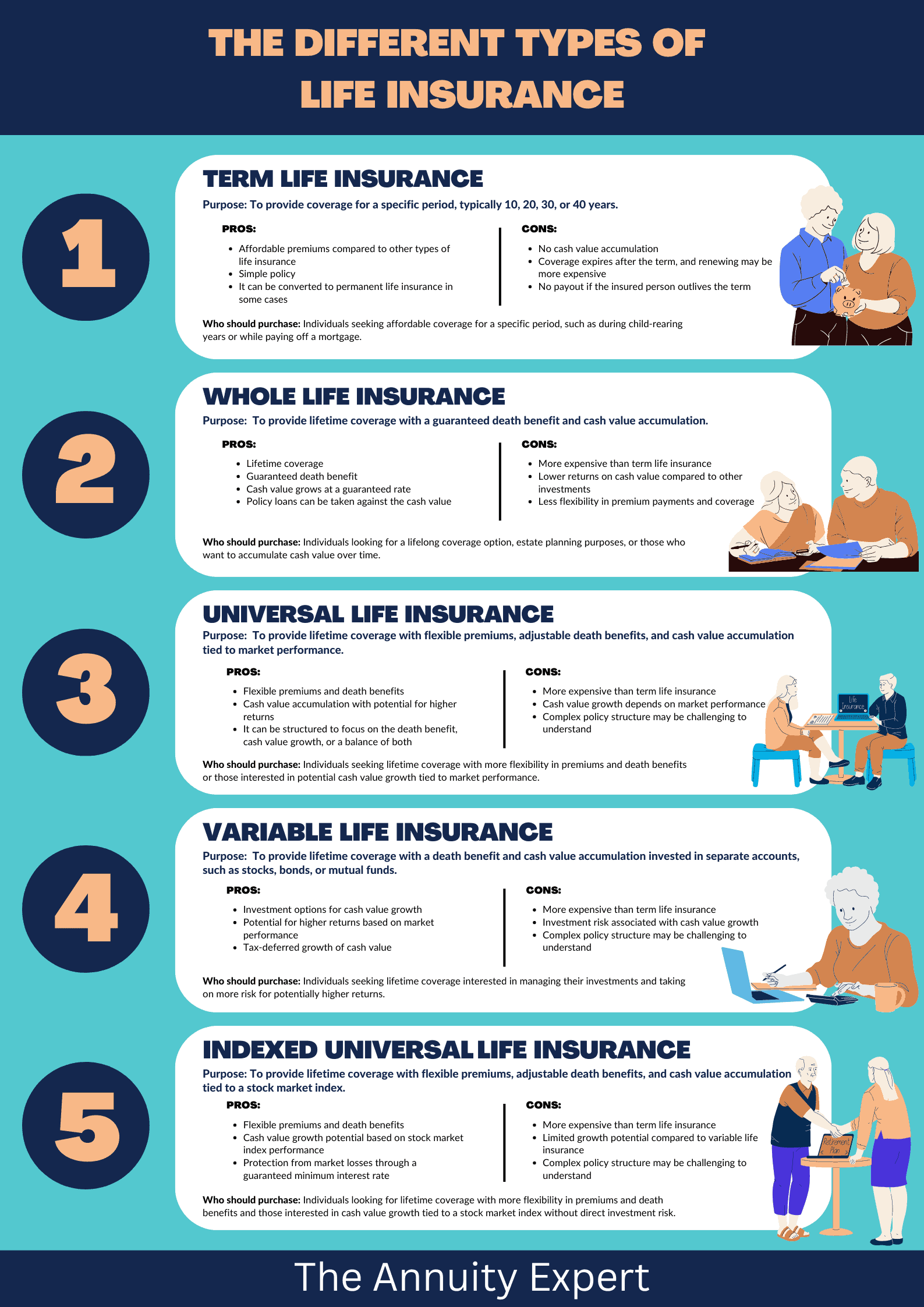

Is Whole Life Insurance Worth the Investment?

When considering whole life insurance, it's essential to evaluate both its benefits and drawbacks to determine if it is worth the investment. One of the primary advantages of whole life insurance is that it provides lifelong coverage, ensuring that your beneficiaries receive a death benefit regardless of when you pass away. Additionally, whole life policies accumulate cash value over time, which can be borrowed against or withdrawn under certain conditions. This feature can serve as a financial safety net, offering policyholders a way to access funds for emergencies or opportunities.

However, investing in whole life insurance often comes with higher premiums compared to term life insurance. The initial costs can be a significant barrier for some, and not everyone may benefit from the cash value component, especially if they don't need lifelong coverage. It's crucial to weigh these factors against your financial goals. Ultimately, the decision should hinge on your long-term plans, current financial situation, and whether the advantages of whole life insurance align with your needs.

Understanding the Benefits and Drawbacks of Whole Life Insurance

Whole life insurance offers several benefits that make it an appealing choice for individuals seeking long-term financial security. One of the primary advantages is the guaranteed death benefit, which ensures that your beneficiaries receive a predetermined amount upon your passing. Additionally, whole life insurance policies accumulate a cash value over time, allowing policyholders to borrow against it or withdraw funds if needed. This feature not only provides a safety net during emergencies but also serves as an excellent tool for financial planning. Furthermore, whole life insurance premiums are fixed, meaning they won't increase as you age, providing predictability in budgeting.

However, it is essential to consider the drawbacks of whole life insurance as well. Primarily, the initial premiums can be significantly higher compared to term life insurance policies. This cost may deter some individuals from pursuing this type of coverage. Additionally, the cash value accumulation is relatively slow in the early years of the policy, which can be disheartening for those expecting immediate returns. Lastly, if you decide to surrender your policy, you may face surrender charges and not receive the full cash value you anticipated. Weighing these pros and cons is crucial for anyone considering this financial product.

Whole Life Insurance vs. Term Life: Which Is Right for You?

When considering whole life insurance versus term life insurance, it's essential to understand the key differences that cater to different financial needs. Whole life insurance provides lifelong coverage and includes a cash value component that grows over time. This can serve as a savings mechanism, making it an attractive option for those looking for stability and long-term investment. On the other hand, term life insurance offers coverage for a specified period, typically 10, 20, or 30 years, and is usually more affordable. This option is ideal for those who need coverage for a specific period, such as during the years when children are dependent or a mortgage is being paid off.

Ultimately, the decision between whole life insurance and term life insurance depends on your individual financial situation and goals. If you seek a policy that builds cash value and lasts throughout your lifetime, whole life insurance may be the better choice. However, if you're primarily concerned with providing financial security for your loved ones at a lower cost for a limited time, term life insurance could be the right fit. Assess your needs carefully, and consider speaking with a financial advisor to make a well-informed choice that aligns with your personal circumstances.